Long-term part-time (LTPT) employment eligibility is a topic that has become increasingly relevant in recent years.

Many individuals work part-time for various reasons, such as interships, contract work or to supplement their income. Many companies also ?have a tendency to hire seasonal workers and retain them on an annual basis. These situations may deem someone eligible to be classified as long-term part-time. However, the question of eligibility for LTPT employment depends on a variety of factors.

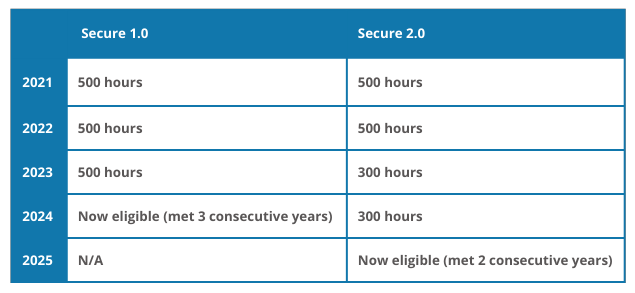

Historically, part-time employees have had difficulty meeting requirements to participate in company retirement plans. Under the SECURE Act of 2019 (or SECURE 1.0), individuals who worked at least 500 hours in three consecutive years are now eligible to participate in a retirement plan.

Additional Legislative Changes

Secure Act 2.0 passed a provision that builds on the SECURE Act requirement allowing increased eligibility for long-term part-time workers to participate in employer-sponsored plans.

- Employers need to start counting hours for part-time employees dating back to Jan. 1, 2023.

- The first date that eligible long-term/part-time employees must be offered participation is Jan. 1, 2025, two years following the start date for counting hours.

- An employee must complete either 2 consecutive years of service (where the employee completes at least 500 hours of service) or 1 year of service (with the 1,000-hour rule).

Who Will Be Affected?

401(k) and 403(b) plans that are subject to ERISA will be required to adhere to the new rules.

Business Owners

- Employers have the option to apply more favorable eligibility provisions for LTPT employees, such as minimum age and eligibility service. This can help to ensure that these employees have access to retirement savings opportunities and can help to improve employee retention.

- Employers have the discretion to make employer contributions for LTPT employees. This can help to incentivize participation in the plan and help to boost retirement savings for these employees.

- Employers don’t have to worry about LTPT employees affecting non-discrimination testing as they have the ability to exclude them. This can help to keep the retirement plan compliant.

- Employers must recognize that both the new two-year rule and the older three-year rule are currently in place. As a result, employees who qualify for the previous rule must be allowed to defer in 2024.

Employees

- The provision allows LTPT employees meeting eligibility requirements to participate in a 401(k) or 403(b) plan subject to ERISA to make deferral contributions. This can help these employees to achieve their financial wellness goals and provide more opportunities for retirement.

I HAVE LTPT EMPLOYEES. WHAT DO I DO?

OPERATIONAL FAQS

Do I need to give LTPT Employees any notices or disclosures on or before their entry date?

Yes. Just like your employees who become eligible due to your plan’s standard eligibility rules or the Year of Service rule, LTPT employees need to receive certain notices and disclosures on or before their plan entry date including:

- Summary plan description

- Participant Fee Disclosure Notice

- QDIA Notice (if applicable)

- Automatic enrollment notice (if applicable)

- Combined automatic enrollment /safe harbor notice (if applicable)

If your plan is a 401(k) safe harbor plan but does not include an automatic enrollment provision, LTPT Employees do not need to receive the safe harbor notice.

Does the plan’s normal age requirement apply?

Yes, an employee must still meet the age requirement in the plan document before they can defer.

Do the new rules apply if my plan excludes part-time, temporary, or seasonal workers?

Yes. They will enter the plan the earlier of 1) completion of a Year of Service (e.g., 1,000 hours in an ECP), or they work three consecutive ECPs, with at least 500 hours in each ECP.

Do these rules apply if my plan has immediate eligibility for 401(k) deferrals?

No, if all your employees are immediately eligible, none will be categorized as LTPT employees.

Are any employees excluded from the LTPT eligibility rules?

Yes, Union Employees, Non-resident aliens with no U.S. source income, and employees who are excluded because of a classification other than part-time, seasonal, or temporary employees, are not subject to the LTPT eligibility rules.

If my plan has automatic enrollment and/or escalations, will it apply to the LTPT employees?

Yes. Plans with the automatic enrollment and automatic escalation provisions will follow the same rules they do for non-LTPT employees. Employees who meet the LTPT eligibility requirements must be automatically enrolled on their plan entry date if they have not made a different election.

- If your plan has an automatic enrollment provision, it is imperative that you provide the auto-enrollment notice to all employees eligible due to the LTPT rules at least 30 days in advance of their entry date, and auto-enroll them into the plan if they do not make an alternative election.

Are LTPT Employees eligible for employer contributions?

No, LTPT Employees are only eligible to make elective deferral contributions. They will not be eligible for employer match or nonelective contributions, including any Safe Harbor contributions. LTPT Employees must meet the plan’s standard eligibility requirements or the Year of Service requirement to be eligible for employer contributions.

If a LTPT Employee’s hours drop below 500 hours in an ECP, do they continue to be eligible to defer?

Yes. They are still considered a participant in the plan and can continue to defer.

Do long term employees accrue vesting years of service?

Yes. The SECURE Act requires LTPT employees to be credited with a vesting year of service for any vesting computational period in which they work at least 500 hours (versus the normal 1,000 hours). Only vesting computational periods beginning on or after 1/1/2021 are considered.

If an employee who became eligible under the LTPT rules later meets the plan’s standard eligibility requirements or the Year of Service rule, they will continue to earn a vesting year of service for each period they work at least 500 hours.

What happens if we fail to offer the plan to an LTPT employee when they become eligible?

If you fail to offer an LTPT Employee the opportunity to defer on their entry date, the plan will have an operational failure that will need to be corrected under EPCRS. Depending on how long they were kept out of the plan after their entry date, this may mean you owe the LTPT employee a “missed opportunity QNEC (Qualified Nonelective Contribution).”

Next Steps

The LTPT rules may seem complicated and overwhelming for business owners. However, with proper planning and communication with your plan’s service providers, you can stay ahead of any necessary changes to plan design, current processes, and systems. At Leading Retirement Solutions, our team of experts can work with you to develop a comprehensive understanding of your plan and ensure that you are in compliance with all regulations.

For tips and information regarding retirement plans, contact us.